W-9 Forms: An Essential Guide for Small Business Owners

Learn when you need a W-9, how to complete it, and why it matters for your small business success in 2026

Tax documents can be confusing. They’re often long, complicated, and packed full of dense terminology—so much so that it can feel like you need a degree in accounting to fill one out. When you’re juggling all the responsibilities that come with being a freelancer or small business owner, this can be a major headache.

Fortunately, the W-9 form—one of the most common you’ll see as a 1099 contractor—is not one of these long, complicated forms. However, if you’ve never seen one, you might have some questions. Let’s explore the W-9 and unpack all the details you’ll need.

What is a W-9 form?

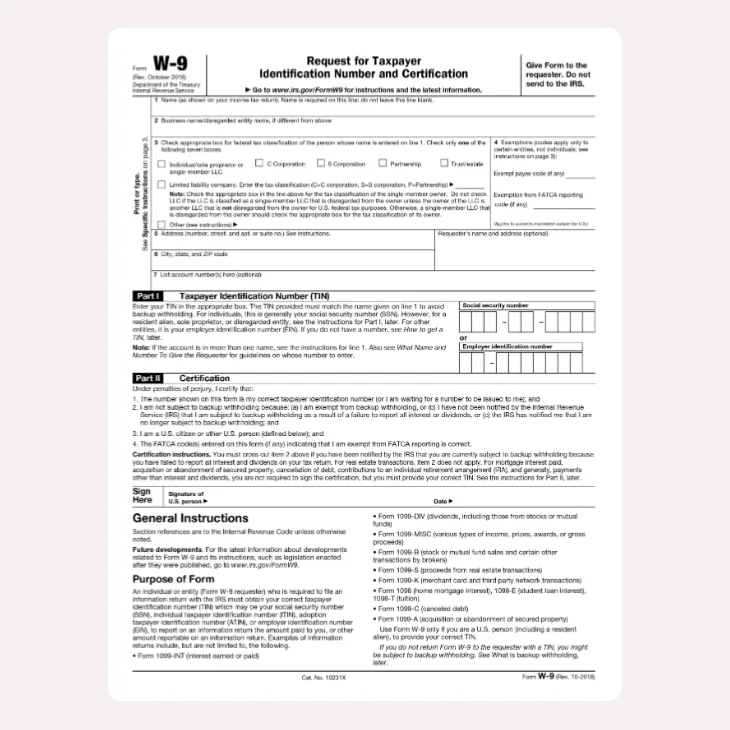

A W-9 form is one of the shortest and usually considered simplest small business tax forms. Form W-9 provides your taxpayer identification number to a client, bank, or other financial institution.

Your taxpayer identification number, or TIN, is the number the IRS uses to uniquely identify you in its system. For most freelancers, it’ll take one of two forms: your Social Security Number or an Employer Identification Number (EIN).

If you do business as a sole proprietor under your own name, you’ll simply use your social. If you operate as a sole proprietor under a different name, or have another business structure, you’ll have an EIN that you provide. You can apply for an EIN online if you don’t have yours yet.

As a freelancer or independent contractor, you’ll often fill out a W-9 for new clients or customers when you first start working with them. This, in turn, enables them to send you a 1099-NEC form, which you submit to the IRS when you file your small business taxes each year.

Who needs to fill out a W-9?

There are a few situations where you might need to fill out a W-9 form:

- Companies may request a W-9 from contractors or freelancers getting paid more than $2,000 per year. This is the threshold where the client will need to send you a 1099-NEC form, and the completed W-9 is required on their end to do this. Any client that falls into this category should be requesting a W-9 from you—if they don’t, you might want to remind them.

- Banks may request a W-9 from you if you’ll be earning interest or other income. This is because the bank will need to submit a different 1099-INT form to report this income. Some banks may also request a W-9 when you open a new account.

- Creditors may request a W-9 when a debt is forgiven or canceled. The creditor will need to file a 1099-C, and—you guessed it—will need a W-9 form to do so.

For most freelancers, the first scenario will be the most common by far. It’s not a bad idea to keep a copy of the W-9 form saved somewhere so you can get it handled quickly on request.

How to fill out a W-9 Form, Step by Step

Compared to many IRS forms, the W-9 is a breath of fresh air. It consists of just three sections to fill out: some basic information, your TIN, and a signature.

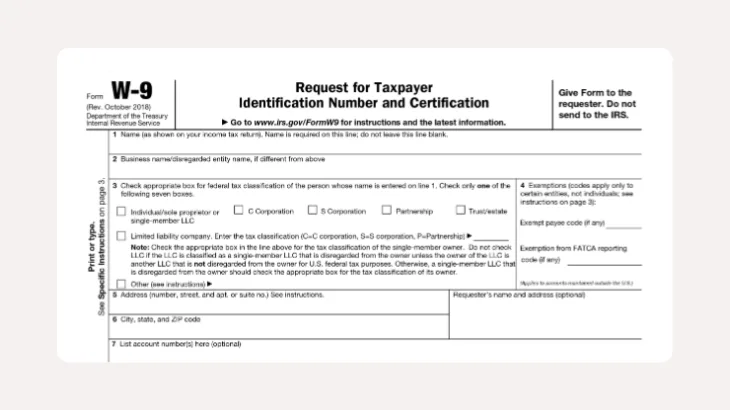

Personal information

The first part is simple personal info:

- Your full, legal name. Print your name as shown on your tax return.

- Your business name. If you operate under a business name or disregarded entity name, print it here. If you operate under your personal name, leave this line blank.

- Your federal tax classification. Here, you’ll check the option corresponding to how your business files taxes. In case you’re not sure, we’ll run through the options:

- Individual/sole proprietor or single-member LLC: If you haven’t incorporated your business and don’t have a partner, you’re probably a sole proprietor. Most (but not all) freelancers will fall into this category.

- S Corporation: S corporations are incorporated pass-through entities—in other words, you’d only pay taxes once rather than twice (like a C corp).

- C Corporation: C corporations have shareholders and a board of directors and pay taxes separately from the owners. If you’re a C corp, you probably know it.

- Partnership: Partnerships are pretty self-explanatory. It’s an unincorporated business owned by two or more people.

- Trust/estate: If you are filling out the form on behalf of a trust or estate, you’ll check this box.

- Limited liability company (LLC): An LLC acts like a corporation at the state level but is taxed like a sole proprietorship at the federal level. This is probably the second most common form a freelance business takes, since many small businesses are LLCs for liability purposes.

- Other: This option is for international business entities.

- Exemptions: If you’re exempt from backup withholding or FATCA reporting, fill out the appropriate space. If you’re not sure, it likely doesn’t apply to you.

- Your address: Enter your address.

- City, state, ZIP: Finish entering your address!

- Account numbers: This only applies if the requester needs certain account numbers from you. If unsure, check with the person or organization requesting the form.

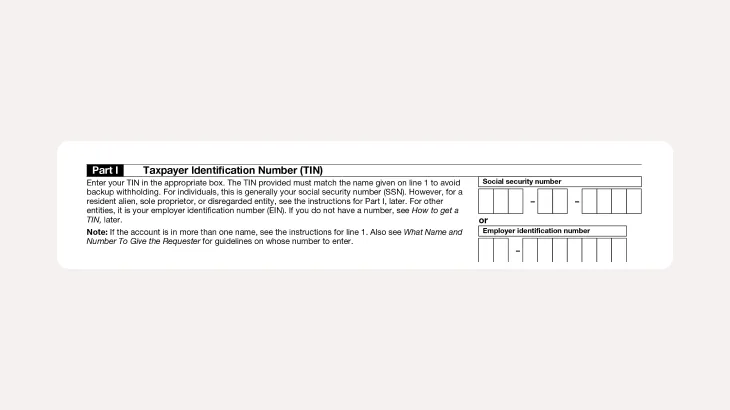

Part I

Now we get to the good stuff—the reason someone requests a W-9 in the first place. In this section, you’ll either enter your Social Security Number or EIN, depending on which applies.

If your business has employees or operates as a corporation or partnership, you probably have an EIN that you use to file taxes. If you operate as a sole proprietor, you may or may not have an EIN, but you can enter either that or your social here.

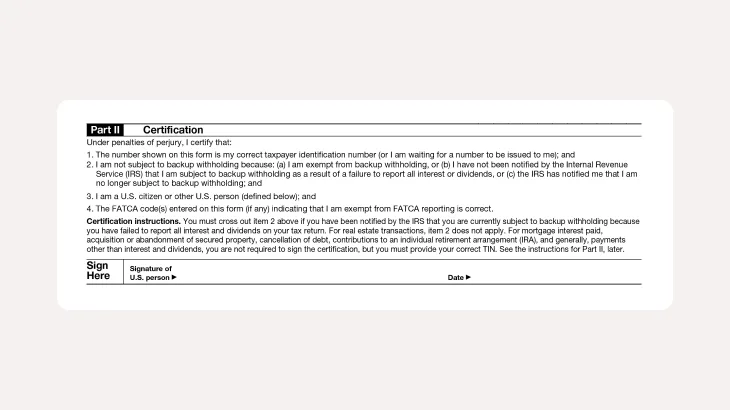

Part II

Finally, you’ll certify that the above information is all true and correct. Simply sign and date the form. Piece of cake!

When should you use a W-9 form?

Generally, you’ll fill out a W-9 form on request by a client, customer, or financial institution. When requested, you should try to get the form returned as quickly as possible—while there’s no deadline from the IRS’s perspective, getting this taken care of quickly will help ensure you receive important tax forms in a timely manner.

What’s the difference between a W-9 and a 1099-NEC?

There’s sometimes some confusion about the differences between these two common tax forms. The easiest way to remember the difference is that you fill out the W-9, but your client fills out the 1099-NEC form.

In other words, you fill out the W-9 and provide it to your client. The client then uses that information to fill out a 1099-NEC form, which reports your yearly earnings from the client to the IRS. They’ll send you a 1099-NEC form for the tax year you completed the work before the IRS deadline, typically in January of the following year.

What’s the difference between a W4 and W-9?

Another form commonly confused with the W-9 is the W-4. A W-4 is a form used by W-2 employees to tell their employers how much money they should withhold for taxes. A W-9, on the other hand, is used by contractors to provide tax identification numbers to a client.

What’s the difference between an I-9 and W-9?

The main difference between an I-9 and W-9 form is who they are intended for. The I-9 form is used by employers to verify the identity and employment eligibility of their employees, while the W-9 form is filled out by independent contractors to provide their taxpayer information to clients. So, while the I-9 form focuses on employee verification, the W-9 form is all about ensuring smooth tax reporting and compliance for small business owners.

Get even more accounting help with Found

The W-9 form is refreshingly simple compared to most tax documents. All you really need to fill it out is your basic personal information, your social security number or EIN, and a pen. Don’t you wish all your accounting was this easy?

Simplify your financial management as a small business owner by harnessing the power of Found’s tools. With Found, we’ll automatically create a pre-filled W-9 form for you. You can confirm everything looks good, then share it via a secure link. You can also manage and remove access to your W-9 at any time to keep your information secure.

If you hire 1099 contractors, you can also request their W-9 forms within Found. Streamline your accounting processes, track income and expenses, and even set aside funds for taxes automatically. Sign up and take control of your financial future.