1099-NEC Instructions Explained: What is Non-Employee Compensation?

Find out the meaning of non-employee compensation and learn how to interpret the IRS 1099-NEC instructions for tax compliance purposes.

Form 1099-NEC is a critical tax document for self-employed people, replacing the 1099-MISC as their equivalent to the employee’s W-2 in 2020. In 2024, the Internal Revenue Service (IRS) expects to receive 83.2 million copies of the form.

Despite their prevalence, you may still have questions about the 1099-NEC instructions or the meaning of non-employee compensation (NEC). If you’re a small business owner, here’s what you should know about them both to stay on top of your obligations.

What is a 1099-NEC?

A 1099-NEC is a tax form for reporting payments to independent contractors in exchange for their services. If you pay more than $2,000 in compensation to an individual who isn’t your employee, you generally must send a 1099-NEC to them, the Internal Revenue Service (IRS), and sometimes a state tax department.

Not only does that help self-employed people track their taxable income, but it also helps federal and state tax agencies ensure taxpayers report their earnings accurately. If you fail to claim all the income on the 1099-NECs you get, they may suspect you’ve underreported your earnings and investigate.

What is Non-employee Compensation?

Non-employee compensation is generally synonymous with self-employment income. It refers to payments made for the business services of someone who is not an employee. Some common examples of NEC include:

- Professional service fees paid to a lawyer or accountant

- Referral fees paid from one professional to another

- Travel reimbursements for an independent consultant who didn’t provide an itemized accounting of the expenses

The IRS offers the following tests to help you determine whether payments are potentially reportable as NEC:

- The recipient is not the payer’s employee

- The payment is to an individual, partnership, or estate

- The payment is for services rendered for a business (includes government agencies and nonprofit organizations)

Notably, payments to corporations are excluded from NEC unless they’re for legal services, including payments to limited liability companies (LLCs) that have elected C Corporation or S Corporation tax structure.

Some other notable payments that don’t constitute NEC include rent paid to property managers, payments made for personal reasons, and payments made via third-party networks like Stripe that get reported on Form 1099-K.

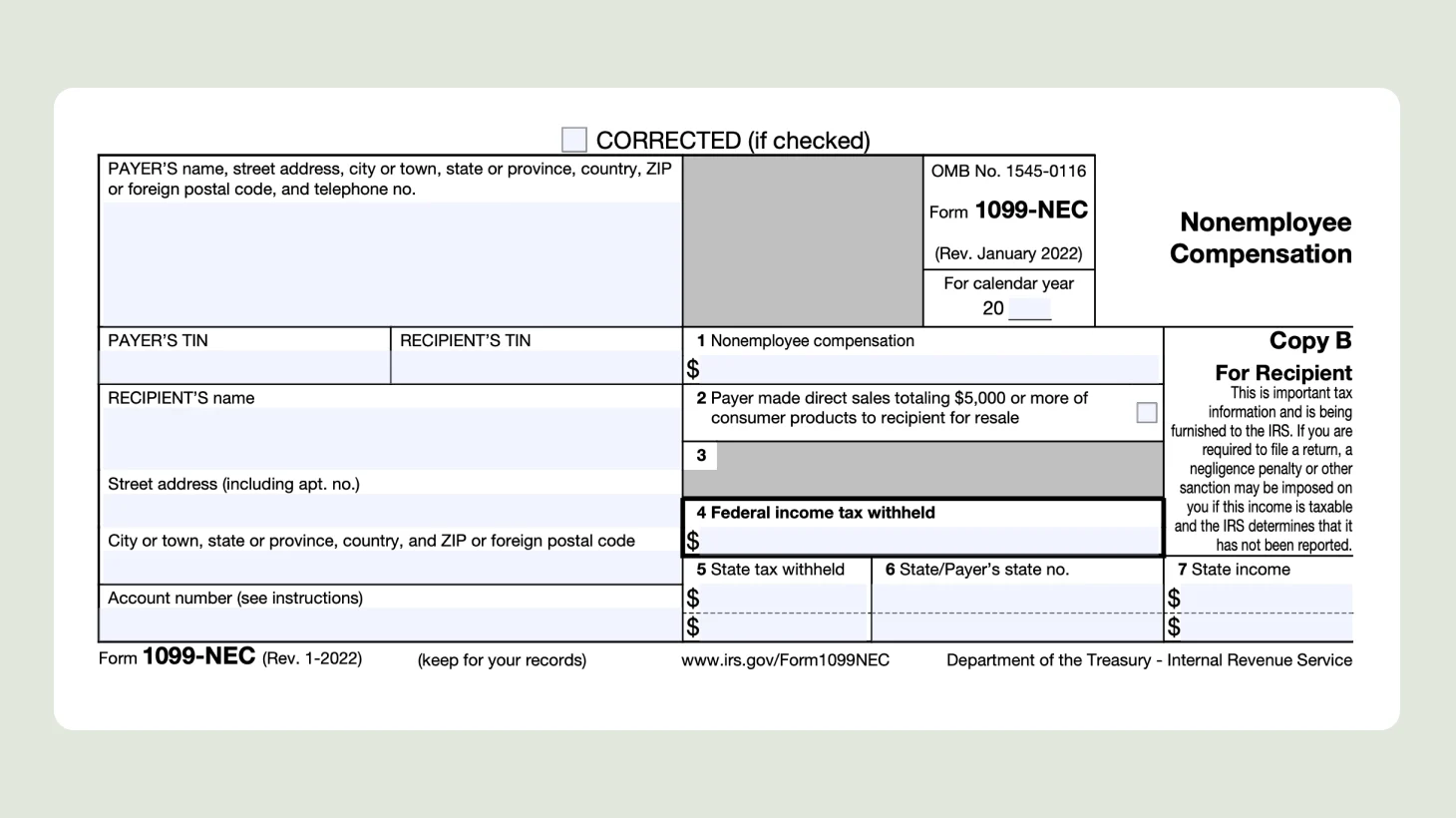

Blank 1099-NEC form

If you’re wondering what Form 1099-NEC looks like, here’s an example of a blank version:

You can only use this copy of the form, Copy B, to complete your responsibility to notify the payment recipient. You must use different copies, Copies A and 1, to fulfill your obligations to tax agencies. We’ll talk more about how to do that in the next section.

1099-NEC instructions explained

The IRS’s 1099-NEC instructions can be tricky to interpret, so here’s a simplified explanation of the most important points.

Who must file a 1099-NEC form?

Businesses, nonprofits, and government agencies that pay at least $2,000 in non-employee compensation to an independent contractor must send them a 1099-NEC form and file a separate copy with the IRS. Some states also require separate copies.

A common misconception is that the payment recipient is responsible for filing the form, but that’s not true. If you’ve collected $2,000 in non-employee compensation from an organization, expect to get a completed 1099-NEC from them. Your only responsibilities are to use the form’s details to help file your taxes and retain it for your records.

If you’re unsure whether payments you’ve made require you to file a 1099-NEC, consider asking a Certified Public Accountant (CPA) for confirmation. They’ll be able to explain your responsibilities, and any payments to consult them are likely tax-deductible.

Who gets a 1099-NEC?

Independent contractors who receive more than $2,000 in non-employee compensation from a business should get a 1099-NEC from the business. The IRS should also get a copy, which it typically forwards to any relevant state tax agencies.

How to fill out 1099-NEC forms

If you paid $2,000 or more in non-employee compensation to a single party during a tax year, here’s how to fill out a form 1099-NEC for them:

- Box 1: Report the total amount of non-employee compensation paid.

- Box 2: Check the box if you sold $5,000 or more in consumer products to the recipient of the non-employee compensation (not typical).

- Box 3: Leave this box blank.

- Box 4: Report any federal income tax you withheld from your NEC payments to the independent contractor (not typical).

- Boxes 5 to 7: These boxes are optional. If your state tax department requires you to file a paper 1099-NEC, fill them out on Copy 1. Report the NEC payment amount in Box 7, any state taxes withheld in Box 5, and the abbreviated name of the state plus your state ID number in Box 6.

You must also provide certain information about yourself and the recipient to complete the 1099-NEC. That includes your addresses and taxpayer identification numbers, such as your Employer Identification Numbers (EIN). To get the recipient’s details, ask them to complete and return a W-9 form.

Lastly, the account number box is typically only necessary to fill out when you’re filing more than one Form 1099-NEC for a single recipient in a given year, which isn’t common.

How to file a 1099-NEC

If you’re required to send a 1099-NEC to a payment recipient, you must also file a separate copy with the IRS. One of the easiest methods is to e-file your information returns through the Information Returns Intake System (IRIS).

To access IRIS, you must apply for a transmitter control code (TCC), which identifies your business when you e-file forms. You’ll need the following information to complete the application:

- Your organization’s EIN

- Your organization’s legal business name, business type, physical and mailing addresses, and phone numbers

- Information about Responsible Officials, Authorized Delegates, and Contacts

- Which information forms you’ll be filing

- The transmission methods you’ll use to file

Processing the application can take up to 45 business days. If you’re up against the filing deadline or prefer to outsource the process, you can pay a third-party filing service or your CPA to handle filing for you.

You may also have to submit a separate copy of the 1099-NEC to the state where you operate, so double-check your local requirements.

When are 1099-NEC forms due?

The 1099-NEC deadline is January 31 following the relevant tax year. For example, 2024 1099-NEC forms are due on January 31, 2025. Most states use the same filing deadlines except for Iowa and Idaho, where forms are due February 15 and February 28, respectively.

You can request an extension by filing Form 8809 to receive an extra 30 days.

What happens if you don’t file 1099-NEC forms?

If you fail to file a required 1099-NEC form by the deadline, you’ll typically get a notice from the IRS notifying you that you owe a penalty. The amount depends on how long it takes you to file.

Here are the penalties for 2024:

- Up to 30 days late: $60

- 31 days late through August 1: $120

- After August 1 or not filed: $310

- Intentionally disregarded: $630

Additionally, interest will accrue on your outstanding penalty balance until you pay off the amount.

How to report 1099-NEC on a tax return

Whether you send or receive a 1099-NEC, you must report it on your annual tax return. If you’re the payer, you should claim the amount in Box 1 as a tax-deductible expense, commonly shown as professional services.

If you’re the recipient, the amount in Box 1 typically constitutes self-employment or business income for you. Assuming you’re a sole proprietor, you should claim it on Schedule C, Line 1.

Streamline your taxes with Found

Managing information returns like 1099-NEC forms can be a surprisingly time-consuming aspect of tax compliance. You’d probably rather focus on running your business, but they’re not something you can afford to ignore.

Fortunately, Found can help you streamline many aspects of the process, significantly reducing the back-and-forth that usually goes into managing 1099s. For example, Found has features dedicated to helping you:

- Send and receive W-9 forms with other businesses via secure links

- Track all payments made to independent contractors through Found’s platform

- Generate complete copies of 1099-NEC forms for each contractor paid $2,000 or more during a given tax year

Say goodbye to the stress of juggling 1099 forms and spend more time on the work most fulfilling to you—which probably isn’t paperwork. Sign up for your Found account today!

FAQs

What does NEC stand for?

In the context of 1099 forms, NEC stands for non-employee compensation.

What is non-employee compensation?

Non-employee compensation generally refers to payments made to a freelancer, independent contractor, or other self-employed person for their business services. For example, it would include the professional service fees paid to an independent accountant or bookkeeper for maintaining financial records.

1099-NEC vs 1099-MISC: What’s the difference?

The IRS requires businesses to report various payments on Form 1099-MISC, like rents, prizes and awards, and health care payments. Non-employee compensation used to be on the list, but that made the information easy for recipients to miss.

The IRS revised its instructions in 2020 to reduce confusion. It now requires businesses to report non-employee compensation on Form 1099-NEC. With the information on its own form, taxpayers should have an easier time tracking NEC payments.

I received a 1099-NEC, but I am not self-employed?

If you believe you’ve received a 1099-NEC in error, contact the organization that sent you the form and ask them to correct their mistake.

Assuming you don’t operate a business and the payment wasn’t self-employment income, you can also report the amount on your tax return as Other Income on Line 8 of Schedule 1, which won’t cause you to pay self-employment taxes.

Just be prepared to explain the situation to any federal or state tax agencies that inquire, especially if the payer doesn’t address the issue.