Profit and Loss Statements for Small Business Owners

Your Guide to Self-Employed Profit and Loss Statements [Template Included]

With inflation eroding consumer purchasing power and wages still struggling to keep up, Americans are increasingly opening small businesses to pad their wallets. As of April 2024, 54% of Americans report that they adopted a side hustle in the last 12 months to supplement their incomes.

However, even if you only become self-employed to earn some extra cash, you have the same accounting and tax responsibilities as a full-time business owner. As a result, you’re going to want a profit and loss statement to help you stay on top of them.

Let’s explore what you should know about the self-employed profit and loss statement, including how the document works, how to build one, and why it’s so nice to have.

What is a Self-Employed Profit and Loss Statement?

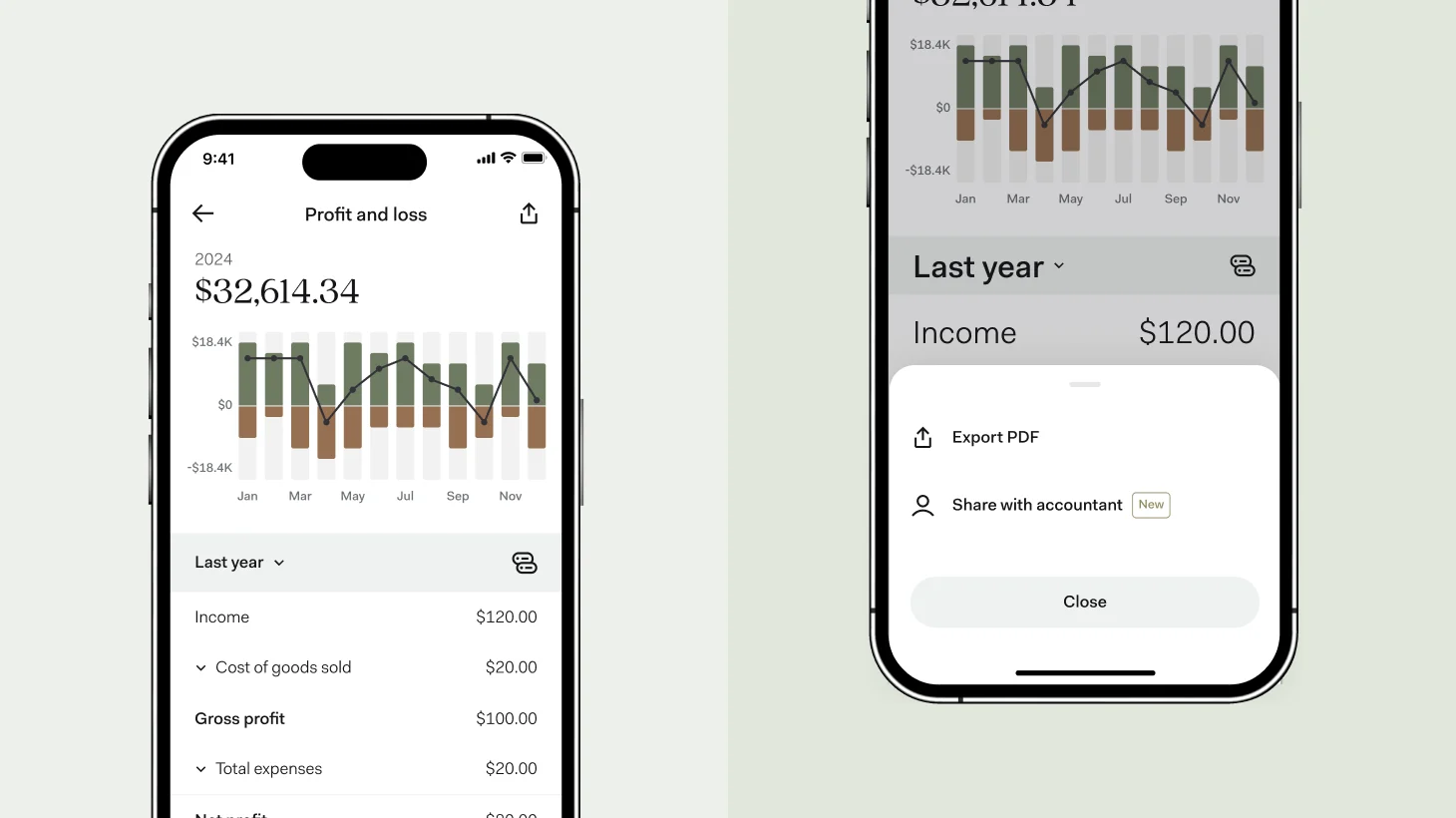

A self-employed profit and loss statement is a report that summarizes your business’s revenues, expenses, gains, and losses over a given period. Also commonly referred to as an income statement, it’s one of two essential financial statements for self-employed people, along with the balance sheet.

Profit and loss statements tell the story of your business operations. They start with your revenues at the top, subtract out your various expenses, factor in any gains or losses, and end with your net profit or loss at the bottom (depending on how things went).

Profit and Loss Statement Structure

All profit and loss statements follow the same fundamental flow, but their structures can still vary between businesses. Most notably, you can use either a single-step or multi-step approach. Here’s how they work:

- Single-step: A single-step income statement gets its name from the fact that it only involves a single calculation: total revenues - total expenses = net profit. It doesn’t differentiate between expense types or break out other profit metrics.

- Multi-step: A multi-step income statement sorts your expenses into categories, like cost of sales and operating expenses. It also involves three separate profit calculations: gross profit, operating profit, and net profit.

A single-step P&L can be easier to produce and might make more sense for a self-employed person who only cares about calculating their net income.

However, a multi-step P&L provides additional insights and is better suited to financial planning. It’s probably worth creating one if you regularly analyze your financial performance and use the data to inform business decisions.

Profit and Loss Statement Components

Self-employed profit and loss statements look different depending on your business activities and accounting preferences, but they share certain common elements. Here are their primary components, listed in the order they appear on the document:

- Revenues: These go at the top of every profit and loss statement. They refer to your gross earnings before accounting for any expenses, though they may factor in things like returns or discounts.

- Cost of Sales: These are the costs that directly relate to making your goods or services ready for sale. For example, if you sell a product, your cost of sales would include the raw materials and labor necessary to build it.

- Gross Profit/Loss: This is the difference between your revenues and your cost of sales. It’s often used to calculate your gross margin, an important benchmark and metric for financial planning that equals gross profit divided by total revenues.

- Operating Expenses: Also commonly referred to as selling, general, and administrative (SG&A) expenses, these are the day-to-day costs your business incurs that aren’t directly related to making a product or service ready for sale. For example, it would include your marketing, interest, professional services, and office supply expenses.

- Operating Profit: This refers to your earnings during a given period after accounting for the cost of your day-to-day operations. It equals your revenues minus your cost of sales and your operating expenses.

- Gains and Losses: These aren’t as common as the other items on this list, only arising when you sell an asset like equipment or a building. They equal the difference between your selling price and the asset’s cost basis. That’s usually how much you paid for the asset, minus depreciation.

- Net Profit/Loss: This is the bottom line of your profit and loss statement. It’s also the ultimate financial result of your business’s activities over the selected period.

Of course, you may not need all of these for your P&L. For example, you might use a single-step income statement, which doesn’t break out gross profit, or you might not incur any gains or losses in a given year.

Why Profit and Loss Statements Matter for the Self-Employed

The profit and loss statement is arguably the most important financial report for self-employed people. It tells you how much revenue you generated, how much money you spent, and what you netted or lost during a given period.

That’s essential for several key business functions, including:

- Gauging your success: Most self-employed people are profit-driven, and a P&L is the only way to track your earnings accurately. You can also use it to gauge your profitability in other ways, like calculating your year-over-year revenue growth rate.

- Financial planning: As your business matures, you’ll face increasingly complex business decisions. For example, you may want to hire additional employees, adjust your pricing strategy, or dial in your budget. Your P&L is an essential tool for that kind of financial planning.

- Tax compliance: Filing business taxes requires that you report your revenues and tax-deductible expenses on the appropriate tax form (most self-employed people use Schedule C). Referencing your P&L for the period makes this process much easier to manage.

You might be able to get away without a formal profit and loss statement in your business’s early days, especially if you have few expenses. However, the report becomes increasingly necessary as your operation grows and becomes more complex.

How to Do a Profit and Loss Statement for the Self-Employed

Fortunately, building a profit and loss statement for your small business has never been easier. Thanks to accounting software, creating an initial P&L statement is usually as simple as linking your business bank account and credit card to a solution.

The software should automatically extract your transactions and use them to generate a preliminary income statement for your business. However, it may not be able to categorize everything accurately for you.

After all, accounting software doesn’t have your insight into your business. It can only sort your income and expenses using the details in your bank statements, such as the name of the merchant involved and the description of each transaction.

It may misrepresent some of your activities as a result. For example, it might categorize all your Amazon payments as Office Supplies expense when you want to record some as Equipment purchases.

Accounting software also isn’t equipped to record certain types of transactions for you, such as:

- Operating expenses you paid for with cash

- Gains and losses from selling fixed assets

- Non-cash expenses, like amortization or depreciation

You, your bookkeeper, or your accountant will need to make adjustments for these kinds of activities to ensure your P&L is accurate. Automation and AI might be able to handle everything one day, but it’s not quite there yet.

If you’ve been avoiding accounting software because you’re trying to keep your expenses down, don’t worry. There are solutions that can generate a P&L statement for you, like Found, which also includes a host of business banking and tax features.

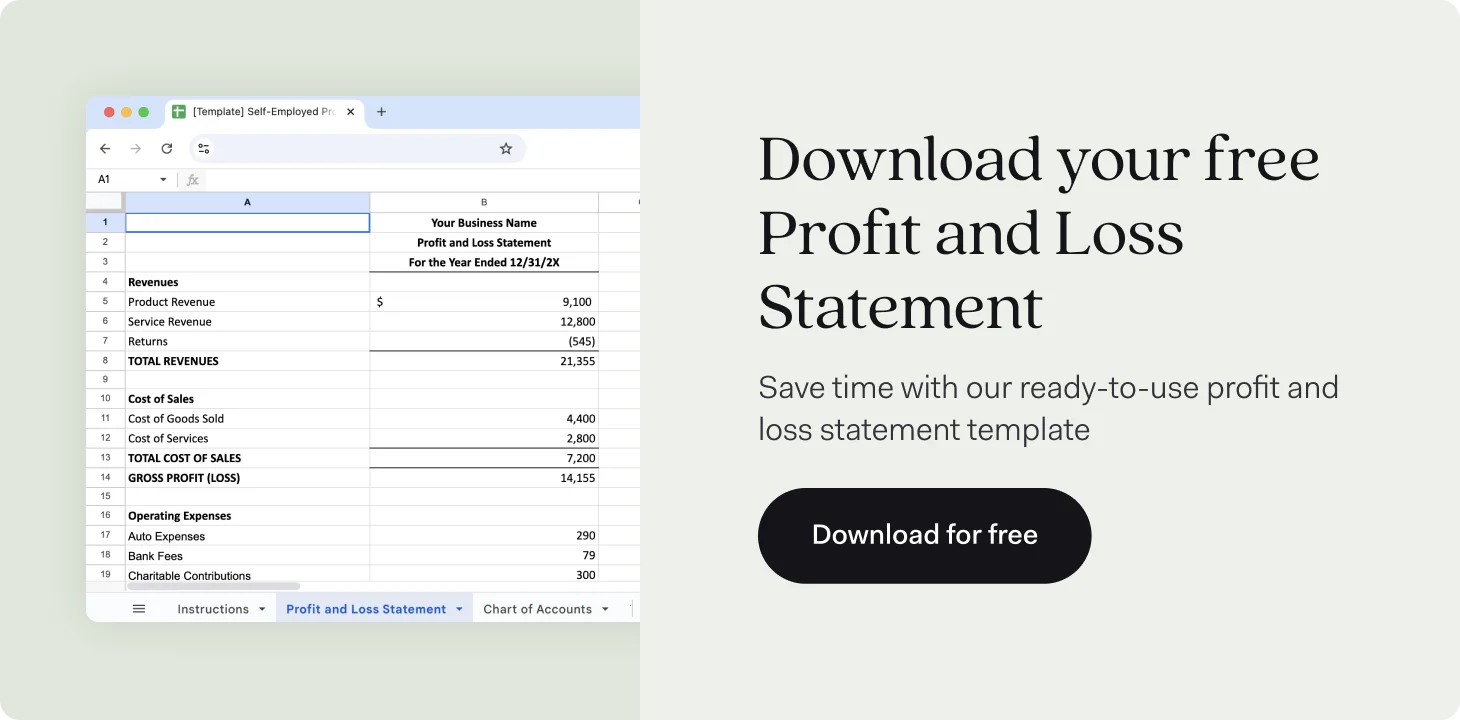

Self-Employed Profit and Loss Template (Google Sheets)

If you prefer working in traditional spreadsheets or aren’t quite ready to delve into accounting tools, that’s fine too. The DIY approach is perfectly valid, and many small business owners still use it.

Fortunately, we’ve got you covered there as well. Check out our Google Sheets profit and loss statement template for the self-employed, built by a Certified Public Accountant.

Once you open the sheet, you’ll want to make a copy for your personal use. Go to the File tab, and then select Make a Copy (4th option)

Create Your Profit and Loss Statement With Found

Found is an all-in-one banking and financial platform designed to make bookkeeping, accounting, and taxes easier for small businesses. In addition to generating a profit and loss statement, Found can:

- Organize your finances with Pockets, subsidiary accounts where you can store funds for various purposes, then spend via Pocket-specific cards

- Use your income and expenses to calculate your tax liability and automatically set aside cash to cover your quarterly estimated tax payments

- Support accountant access and allow both parties to leave comments for each other, reducing the need for meetings and back-and-forth emails

Found can conveniently satisfy your business banking and accounting needs at once, streamlining your systems and saving you from juggling multiple solutions. Sign up for your Found account today!

FAQ

Is an Income Statement the Same as a Profit and Loss Statement?

Yes, an income statement is the same as a profit and loss statement, and you can use the two terms interchangeably. They both refer to the financial statement that summarizes your business’s revenues, expenses, gains, and losses over a given period, culminating in your net profit or loss.

What is PNL in Business?

PNL is another way of saying P&L, which is short for profit and loss. It typically refers to the profit and loss statement. That’s one of the primary financial statements for the self-employed, alongside the balance sheet and sometimes the statement of cash flows.

What is P&L Management?

P&L management refers to analyzing your income statement and using the insights to make more profitable business decisions. For example, you might engage in variance analysis by comparing your budgeted and actual expenses. If you discover any overspending, you can look for opportunities to cut costs or adjust your budget.

How Often Should a Business Calculate Profitability and Review Financial Statements?

You should calculate your profitability and review your financial statements somewhere between every month and every year. The ideal cadence often depends primarily on how much you use recent financial data to inform your business decisions and tax compliance.

For example, an Airbnb host might want to factor their previous month’s bookings into their nightly rates, while an Uber driver might only need to review their financial statements when they’re preparing to file their annual taxes.