What to Know about Retirement Plans When You Own a Small Business

Even though you might love your job, nobody wants to work forever—and nobody should. That’s why it pays to start saving for retirement, ideally as early as possible.

Many employed Americans are familiar with the retirement world’s most common offerings. In fact, about 40% of Americans have a 401(K) or Individual Retirement Account (IRA).

However, self-employed Americans—who might be missing out on one or both of these accounts—might be surprised to learn that there are ample options for them to get in on the retirement action, too.

There are also plenty of good reasons to get started now, no matter how many years deep you are in your career.

Why save for retirement?

Though it might not be the sexiest topic, saving for retirement is an essential part of your career—and one that pays to start sooner rather than later.

Thankfully, you’re paying it forward to your future self with every paycheck or quarterly estimated tax payment you make. That’s because a portion of your income taxes pays for Social Security, Disability Insurance, and other entitlement programs.

After working for about 10 years, you’ll qualify for the full value of these Social Security benefits—which you can start taking as early as age 62, at America’s ‘de facto retirement age’ of 65, or as late as 70. You can even check in to see how much progress you’ve made toward being eligible for benefits in the Social Security agency’s online portal.

However, there’s some bad news: your “automatic retirement savings” in Social Security won’t cover all your bills in retirement. Today, a person earning $50,000 per year can expect Social Security to replace just 35% of their income.

And in the current environment, the coverage from Social Security is expected to worsen or potentially go away entirely. Moreover, there are considerable concerns about the program’s long-term viability, so people need to plan now that Social Security benefits might be reduced—or phased out entirely if it isn’t fixed.

That’s to say: you’ll need to find the other 65% of your retirement—or 100% if you’re feeling pessimistic—somewhere else.

The great news is that self-employed people have many opportunities to start putting away money for their future selves, usually in retirement accounts. There’s a huge advantage if you start sooner rather than later.

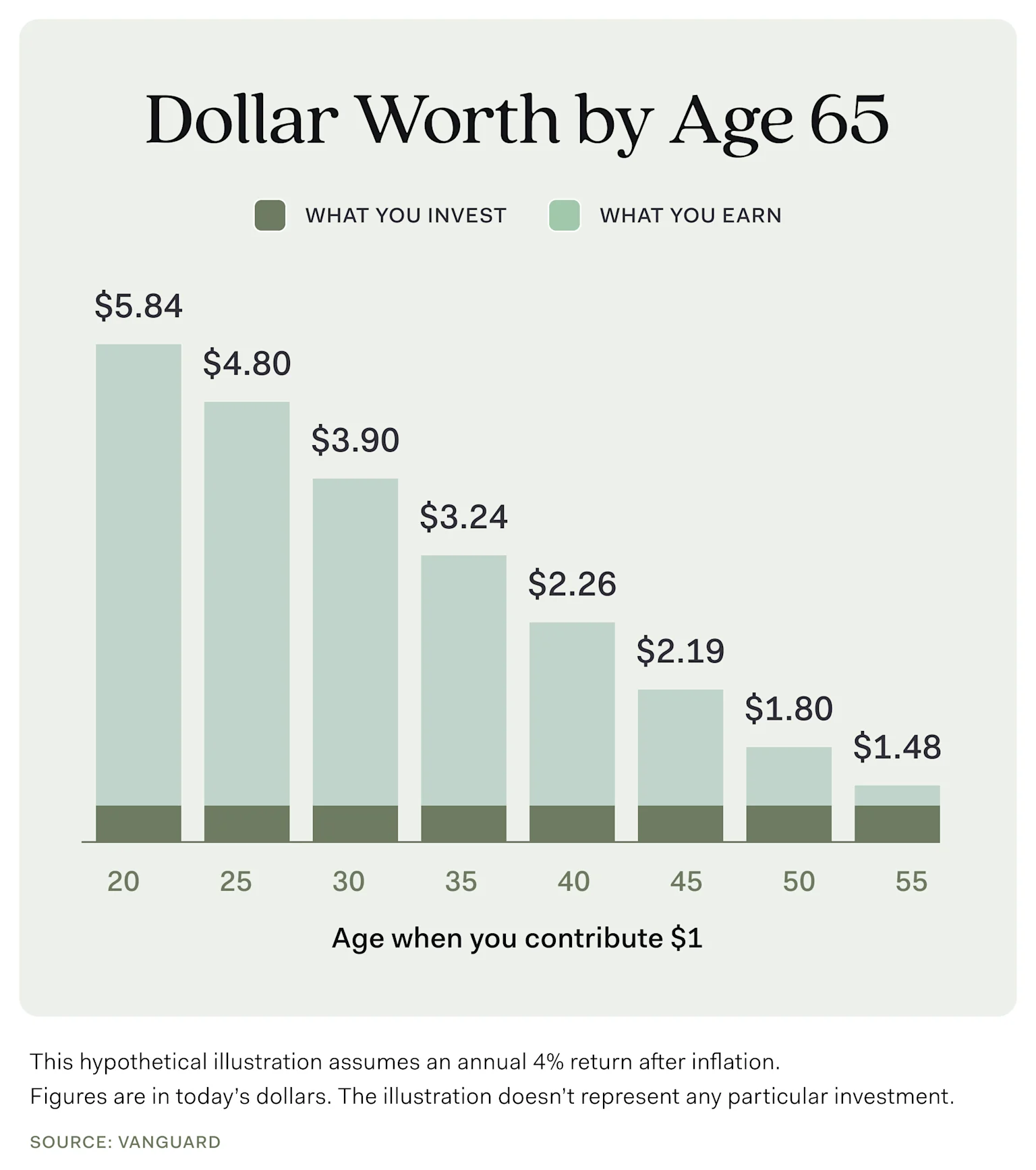

Retirement giant Vanguard shows that a dollar invested by a 20-year-old could turn into as much as $5.84 by retirement. Meanwhile, that same dollar only becomes $1.48 if you start investing at 55. These kinds of returns might feel far-fetched, but they are real possibilities if you start early. To make matters even better, you can be rewarded for investing long-term.

Source: Vanguard

What are the different kinds of retirement accounts?

The most common way people save for retirement is through qualified accounts, commonly known as retirement accounts. Americans use these accounts because they confer tax benefits, which could mean tax savings now or later.

Traditionally, the balances of these qualified accounts are spread into investments like stocks and bonds. These investments are known to appreciate faster than cash, which makes them preferable for long-term investors who aren’t afraid of some risk. The ratio of these assets is decided by a financial planner, your employer, a roboadvisor, or even yourself.

Individual Retirement Accounts

Many Americans starting their retirement journey start with an Individual Retirement Account (IRA.)

IRAs are an account you can set up and manage by yourself, allowing you to contribute money towards retirement on your own terms. These are often the natural entry point for many self-employed and traditionally employed people because anybody with earned income can set up an IRA or a Roth IRA.

However, if you surpass the $6,500 annual contribution limit that an IRA offers, you’ll naturally be looking for the next steps—and that’s where employer-sponsored retirement plans come in.

Employer-Sponsored Retirement Plans

Once you’ve climbed the first hill—your individual retirement accounts—your natural next stop will be employer-sponsored retirement plans.

Most Americans are familiar with the 401(K), the most common retirement plan employers offer. People who have worked for many years might have one or multiple employer-sponsored plans. Some of those include:

- 401(K): A plan where employees can contribute pre-tax employment income for a tax break in the current tax year, but taxed withdrawals in retirement.

- Employees can contribute $22,500 of their paycheck.

- Employees over the age of 50 can contribute an extra $7,500 in ‘catch up’ contributions, or a total contribution of $30,000.

- Generous employers who offer a match or other retirement benefits are allowed to contribute to your plan, too. The total limit of employee and employer contributions can be as high as $66,000.

- Roth 401(K): A plan where employees can contribute taxed employment income for tax-free withdrawals in retirement

- Like its traditional counterpart, employees can contribute $22,500 of their paycheck. Employees over 50 can contribute an extra $7,500 in ‘catch up’ contributions, or a total contribution of $30,000.

- Employers are able to contribute a match or other bonuses to your Roth 401(K) on your behalf, but the total combined value of employee and employer contributions can’t exceed $66,000.

- 457(b) Pension Plan: A fixed plan, usually for deferred income, offered by private or public employers

- You are allowed to defer up to $22,500 of your salary per year, but employers cannot make contributions on your behalf.

- However, contributors between the age of 62 and 65 are able to contribute double the annual contribution limit. This is because 457(b) plans are mostly designed for people nearing retirement, who want to defer their income until a later year to reduce their current-year taxable income.

- You can also stack your unused contribution limits from prior years to your limit if you are between the age of 62 and 65, meaning that you can contribute between $45,000 (twice the annual limit) and $62,500 (assuming you haven’t used your limits from prior years.)

- 403(b) Plan: A plan traditionally reserved for educators and teachers

- Employees are able to contribute up to $22,500 to their 403(b) in 2023.

- Employees over the age of 50 are allowed an extra $7,500 in catch-up contributions, for a total of $30,000 in total employee contributions.

- The combined employee and employer contribution limit cannot exceed $66,000.

- Thrift Savings Plan (TSP): A plan for Federal employees and members of the uniformed services

- Employees are able to contribute up to $22,500 to their 403(b) in 2023.

- Employees over the age of 50 are allowed an extra $7,500 in catch-up contributions, for a total of $30,000 in total employee contributions.

- The combined employee and employer contribution limit cannot exceed $66,000.

If you have a day job with your side gig or freelance ventures, you might have one or multiple accounts above. You might also be able to make the most of your freelance money—whether it’s your main thing, side thing, or only thing—using self-employed retirement plans.

Self-Employed Retirement Plans

If you’re your own employer, don’t fret—you can also make the best of America’s far-reaching retirement plan options for yourself. After all, you are the boss.

There are several accounts self-employed people can use to go the extra mile with their retirement. Those include some fairly familiar names, as well as some unfamiliar ones:

- Solo 401(K): A plan which allows you to contribute pre-tax income from self-employment for a tax break in the current tax year

- Since you’re the employee and employer in a Solo 401(K), you can contribute both the employer and employee portions to your own retirement if your business operates at a profit.

- Employees can contribute $22,500 of their paycheck.

- Employees over the age of 50 can contribute an extra $7,500 in ‘catch up’ contributions, or a total contribution of $30,000.

- If you can afford it, you can also contribute a match or other bonus as your own employer, so long as your total contributions don’t exceed $66,000.

- Solo Roth 401(K): A plan which allows you to contribute taxed self-employment income for tax-free withdrawals in retirement

- Since you’re the employee and employer in a Solo 401(K), you can contribute both the employer and employee portions to your own retirement if your business operates at a profit.

- Employees can contribute $22,500 of their paycheck.

- Employees over the age of 50 can contribute an extra $7,500 in ‘catch up’ contributions, or a total contribution of $30,000.

- If you can afford it, you can also contribute a match or other bonus as your own employer, so long as your total contributions don’t exceed $66,000.

- Simplified Employee Pension Plan (SEP IRA): A plan for self-employed people or small business owners with few employees

- Contributions to your SEP are made exclusively on behalf of your business, whether for yourself or for any employees you have.

- Contributions must not exceed 25% of the employee’s compensation or $66,000 in 2023.

- You must set a contribution rate, which must be the same for any and all employees.

- Savings Incentive Match PLan for Employees (SIMPLE IRA): A plan for self-employed people or small business owners with up to 100 employees

- Contributions to the SIMPLE IRA allow employees to contribute up to $15,500 in 2023.

- Employers must match contributions up to 3% of compensation, which has nop bearings on the annual compensation limit; or offer a 2% nonelective contribution if employees don’t contribute.

- Defined benefit plans: A plan for high-income self-employed people looking to save a lot for retirement

- Defined benefit plans don’t have a fixed formula or way of calculating benefits for plan participants, so an expert is recommended to set this up for a prospective high-earner looking to tap this retirement option.

- Contributions to defined benefit plans cannot exceed 100% of the participant’s average income for the three most recent calendar years.

- Alternatively, the limits cap at $265,000 at 2023.

That’s a lot of information to digest, so you might wonder what your best bet is. We’ve got you covered there:

How should I save for retirement?

This answer hinges on several different factors. How much income do you make? How much do you want to put toward retirement? Are you a full-time freelancer or self-employed individual? Do you work multiple jobs? Do you receive regular income from either w-2 or 1099 work?

When considering these questions, consider consulting a financial advisor or financial planner who can help you navigate these complex nuances.

However, given these considerations, three common situations aspiring retirement savers might fall into based on how much income you make from your freelance work:

- Full-time Freelancers: People who make all (or almost all) their money from self-employment, freelance, or gig work.

- 50/50 Earners: People who make a nearly equal amount of money from their w-2 role and freelance or self-employment.

- Traditional Employees: People who make all (or almost all) their income from a traditional w-2 job, and a lesser (albeit not insignificant) amount from freelance or gig work.

Let’s dive into how each of these different situations might look for you:

Full-time Freelancers

If what you do for yourself is your main thing or the only thing, you might find an IRA/Roth IRA and a low-maintenance plan such as a SEP IRA will be your best bet to approach retirement planning.

The IRA part is easy: choose either a Traditional IRA (deduct your contributions on your taxes now, but pay taxes on withdrawals in retirement) or a Roth IRA (pay taxes on contributions now, get tax-free withdrawals in retirement) and contribute every dollar towards the max.

In the tax year 2023, the max you can contribute to an IRA is $6,500 (or $7,500 if you’re over 50.)

Once you’ve maxed your IRA, if you operate a sole proprietorship or single-member LLC like most solopreneurs, consider opening a SEP IRA. This account type is a no-brainer because of its low administrative burden and high contribution limits.

You’ll be able to contribute up to 25% of your net self-employment income (your company’s income minus its expenses minus half of the self-employment taxes) to your SEP IRA, directly from your company’s balance sheet—which means your retirement contributions can help reduce your company’s net income.

If your business is not profitable for whatever reason, you will not be able to contribute to a SEP or any self-employed plan. Consider this before setting up your SEP.

50/50 Earners

If you have one foot in a w-2 gig (or multiple w-2 gigs) and another foot in the gig or freelance economy, you might have a more nuanced situation than most.

Despite that nuance, you should make your best effort to contribute to a Traditional IRA or Roth IRA, ideally up to the max. That’s because it’s an account that offers the most control and certainty. In the tax year 2023, the max you can contribute to an IRA is $6,500 (or $7,500 if you’re over 50.)

Once you’ve done that, you should take score of what accounts you might have access to already. In a w-2 job, you might be offered a 401(K) or another employer-sponsored plan. More importantly, you might find that your employer offers a match on contributions—which is basically free money for making contributions.

Always prioritize making contributions to retirement accounts with matches or other bonuses. The max amount you can contribute from your w-2 paychecks in tax year 2023 is $22,500 (or $30,000 if you are over age 50.)

If, for whatever reason, you work multiple w-2 gigs and they both offer a 401(K), you can probably contribute to both plans. However, your total 401(k) contributions cannot exceed $66,000 or 100% of your contributions in tax year 2023. Bear in mind, that limit does include your employer match.

In many cases, just focusing on maxing your IRA and a 401(K) will be enough for most—maxing both accounts will set you back a minimum of $29,000.

However, at this level, you might receive a paycheck from their own business.

If that describes you, and you have more than one employee, consider setting up a SIMPLE IRA for your small business and its employees. A SIMPLE IRA allows larger small businesses to make fixed contributions from each paycheck or match a percentage of a paycheck contributed to a retirement account.

As always, consult a tax professional and your company’s respective payroll leaders or human resources before deciding how to structure your annual retirement contributions.

Traditional Employees

If the majority of your money is coming from a single w-2 gig each year, you might choose to max traditional retirement accounts, while maximizing the writeoff value of your self-employed business.

How does this look in practice? Well, like with the two scenarios above, it starts by trying to max an IRA or Roth IRA. Then, if your main gig has a 401(K) or another employer plan, you should contribute your desired amount to that.

However, from there, your efforts are better spent writing off expenses against your self-employment income rather than trying to increase those expenses with a retirement account such as a SEP IRA.

Of course, you could set up a SEP IRA for your side hustle or freelance gig, but writing off self-employment-related travel expenses or software might be better than trying to keep your business in the green to make retirement contributions.

As with anything, consult a tax professional to weigh these considerations with respect to what is important to you.

See the bigger picture before it’s there

Planning for retirement isn’t easy—neither is running your own business. Whether your self-employed work is your main thing, your side thing, or your only thing, you need an ally to set the course for your financial future. Fortunately, there are a lot of great and inexpensive tools out there offering free or low-cost business banking and expense tracking complete with invoice tools and tax write-off tracking so you can manage everything in one place. Learn more about how Found can help you track your income, expenses, and retirement contributions.