How to Budget as a Freelancer: A Step-by-Step Guide

A freelancer’s guide to building a reliable budgeting system for variable income

Your stomach drops when you check your bank account. Three clients haven’t paid. Quarterly taxes loom just 14 days away. Even though you crushed your income record two months ago, you’re back to the “which bill can wait” game.

Freelance life gives you freedom but serves up money stress that regular budget advice doesn’t touch. The system you’ll discover here doesn’t just acknowledge your up-and-down income reality—it works with it.

5 Reasons Managing Money Matters More for Freelancers

When you work for yourself, money works differently. W-2 employees get predictable checks with taxes handled. You don’t. You’re balancing unpredictable cash flow, tax payments, and business costs without help. Here’s why you need your own money system:

- Your bank account looks like a roller coaster: Last month you billed $6,000. This month? Just $2,200 so far. Your money plan must work during feast and famine—something your corporate friends never worry about with their Friday direct deposits.

- The tax clock is always ticking: Miss a quarterly payment and you’ll watch your hard-earned cash vanish into IRS penalty notices. Many freelancers learn this the hard way their first year when they pay an extra $800 for being late. The government wants its cut regardless of whether you had a good month.

- Benefits come from your pocket: Remember company-matched retirement funds? Paid sick days? Health insurance? That’s all on you now. You need cash specifically set aside for these basics that your employed friends take for granted.

- Business and personal money blur too easily: When your business account runs low, your personal credit card looks like a quick fix—but creates tax headaches you’ll spend months untangling. Without clear lines between accounts, you’ll never know if you’re actually making money.

- Getting credit becomes a hard sell: “But how stable is your income?” becomes the soundtrack of mortgage meetings. Smart money habits–and savings–help prove your reliability when standard paperwork can’t tell your whole story.

Standard budget advice assumes steady paychecks. You need something built for the ups and downs of real self-employment.

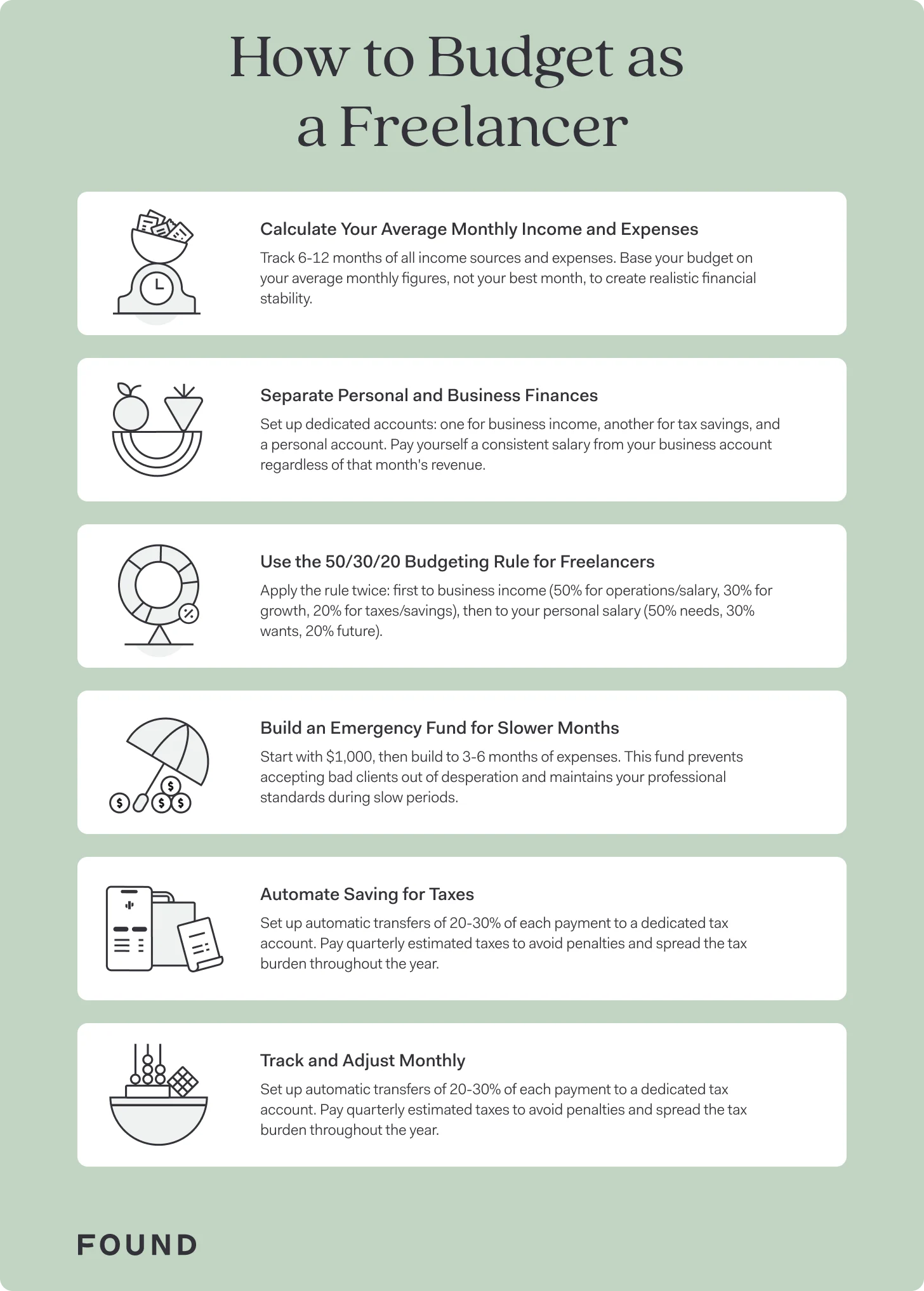

Step 1: Calculate Your Average Monthly Income & Expenses

Before creating a budget, you need to understand your actual financial situation. Don’t make the mistake of budgeting based on your best month, which leads to problems during slower periods. Start with reality, not high hopes.

Start by tracking your:

- Income from all sources over the past 6-12 months

- Fixed expenses (rent, subscriptions, insurance)

- Variable expenses (groceries, entertainment, client meals)

- Business expenses (software, office supplies, professional services)

Add up your total income for the period and divide by the number of months to find your average monthly income. Do the same for your expenses.

Step 2: Separate Personal & Business Finances

One of the biggest mistakes new freelancers make is using a single bank account for everything. This creates tax headaches and makes budgeting nearly impossible.

At minimum, you need:

- A dedicated business checking account for receiving client payments

- A way to save for tax payments (more on this in the next step)

- An emergency fund account

When a client pays you, the money goes into your business account. Then, you pay yourself a consistent amount each month from your business account to your personal account—even if you earned significantly more that month.

Step 3: Use the 50/30/20 Budgeting Rule for Freelancers

The 50/30/20 budgeting rule is a common budgeting approach that allocates 50% of income to necessities, 30% to discretionary spending, and 20% to savings and debt repayment.

For freelancers, this rule needs modification because you manage two separate financial entities.

First, apply it to your business income:

- 50% for business operations and your salary: This includes both essential business expenses (software, insurance, supplies) and the salary you pay yourself. Your personal salary should be your largest business expense, treated as a regular operational cost.

- 30% for business development: Reinvestment in growth opportunities like better equipment, training, or marketing.

- 20% for taxes and business savings: Set aside for quarterly tax payments and build a business emergency fund.

Then, apply it again to your personal salary:

- 50% for personal needs: Housing, groceries, utilities, healthcare, transportation

- 30% for personal wants: Entertainment, dining out, hobbies, non-essential purchases

- 20% for personal taxes and future: Additional tax savings (if needed) and personal retirement contributions

Taking a two-tiered approach ensures that both your business and personal finances remain healthy. Your salary isn’t 50% of your business income—rather, it’s an expense that comes from the 50% allocated to business operations, with the exact percentage varying based on your business model and expenses.

For example: If your business earns $5,000 monthly, you might allocate $2,500 (50%) to operations, including a $1,800 salary to yourself. The remaining $700 covers other essential business costs. Then you apply the 50/30/20 rule to your $1,800 personal salary.

Step 4: Build an Emergency Fund for Slower Months

Saving feels impossible with fluctuating income, but for freelancers, an emergency fund isn’t a luxury—it’s a necessity. But it’s a hard necessity: Research shows 71% of freelancers struggle to save due to unpredictable income, with many facing short-term financial emergencies.

An emergency fund serves an important job for your business:

- Covers gaps between projects

- Prevents accepting bad clients out of desperation

- Maintains your rate integrity during slow periods

- Handles true emergencies without derailing finances

While an emergency fund isn’t built overnight, you can start small with a tiered approach:

- Save $1,000 as quickly as possible

- Build an emergency fund of three months of expenses

- Reach your ideal goal of an emergency fund that can cover six months of expenses

Once you have this safety net, you might find yourself having the freedom to make better business decisions. You won’t take terrible clients out of desperation or undersell your services because you’re worried about making rent.

Step 5: Automate Saving for Taxes

Surprise tax bills have the potential to destroy freelancer finances–especially for those with no savings. Automation creates a protection system by removing the temptation to “borrow” from tax money when cash flow is tight.

Set up these automatic transfers immediately:

- 20-30% of each payment directly to a dedicated tax savings account

- Fixed amounts to business expense accounts for predictable costs

- Consistent contributions to retirement accounts, even if small

Submit quarterly estimated tax payments to prevent penalties and spread the tax burden throughout the year. This approach prevents the cash flow shock of a single large annual payment and helps you stay compliant with IRS requirements.

Step 6: Track and Adjust Monthly

Unlike traditional W-2 employees, freelancers can’t just look at their finances a few times a year. Scheduling regular financial check-ins will allow you to:

- Compare actual income against projected income, as this affects your estimated taxes

- Review upcoming expenses and client payments

- Adjust your personal “salary” if needed

- Check tax savings progress

- Identify expense patterns and opportunities for savings

Whether you do this weekly or monthly, this check-in should help you catch trends before they become major—and costly—problems in the long run. These reviews also help you spot seasonal patterns in your income, allowing you to anticipate and prepare for predictable slow periods rather than being caught off guard.

Hold yourself accountable by scheduling a recurring block on your calendar to do this. Use that time to review your bookkeeping and expenses, send invoices, follow up on outstanding payments, and check in on financial goals.

When to Get Professional Help

While this DIY budgeting system works well for many freelancers, your financial situation will evolve as your business grows. Knowing when to wave your white flag and ask for help often pays for itself through tax savings, better financial planning, and peace of mind. Consider working with professionals when:

- Your annual revenue exceeds $75,000: At this income level, the tax-saving opportunities likely expand significantly. A certified public accountant (CPA) can identify deductions and strategies you might miss, often saving you more than their fee.

- You’re dealing with multiple tax jurisdictions: Working with clients across different states or countries creates complex tax situations. A tax professional who specializes in multi-state or international taxation can help navigate these waters and prevent double taxation.

- You want to establish a more formal business structure (LLC, S-Corp): The right business structure can provide liability protection and tax advantages. A business attorney and a tax professional can guide you through the process of selecting and setting up an entity based on your specific situation.

- You’re planning to hire 1099 contractors: Bringing on help creates new tax obligations and paperwork requirements. A bookkeeper or accountant can help you properly classify workers and manage 1099 filings to avoid costly misclassification penalties.

A good accountant or financial advisor familiar with freelance businesses can often save you more than their fee through tax optimization, financial planning, and helping you avoid costly mistakes. An added bonus? Their fee is also likely a tax-deductible business expense.

Run your business finances with Found

Freelance budgeting isn’t about restriction—it’s about creating financial stability that gives you more freedom to choose projects you love and clients who value your work.

The system outlined here has helped thousands of freelancers transform their financial outlook from constant stress to confident planning. The key is consistency and treating your finances with the same professionalism you bring to client work.

Found is an all-in-one banking and financial platform for small businesses that simplifies taxes, invoicing, and bookkeeping. Key features include automatic tax savings, real-time tax estimates, and built-in expense tracking to maximize deductions. With no required hidden fees or maintenance fees⁴, monthly minimums, or credit checks, Found makes it easy to separate business and personal finances—a critical first step in our budgeting system.