You Got a PPP Loan. Now What?

As small business owners and self-employed people across America start seeing their Paycheck Protection Program (PPP) loan funds hitting their accounts, many folks are asking, “What next?”

Now that you’ve got your loan, you should consider two key things: how to apply for loan forgiveness and think about your PPP loan come tax season.

PPP Loan Forgiveness

Although PPP loans are called “loans,” they are fully forgivable if you satisfy some relatively simple legal requirements.

For PPP loans of $150,000 or less, the Small Business Association (SBA) has created a one-page forgiveness application form, Form 3508S, that you file with the lender who gave you your original loan. You can do this any time after you spend your loan proceeds, within 10 months of your 8 or 24-week spending period.

For larger businesses with employees, forgiveness can be complicated because a business must prove they spent at least 60% of the loan proceeds on employee payroll. The total number of employees on the payroll must also be maintained.

The good news is you don’t have to worry about this if you are self-employed, with no W2 employees. In this scenario, PPP loan forgiveness is actually pretty straightforward.

For a self-employed individual, “Payroll Costs” include all amounts you paid yourself as the owner of your Schedule C business (which the SBA calls “owner compensation”), rent, mortgage interest, business-related software, supplier costs, or Covid-related worker protection measures

When you’re a sole proprietor with no employees, your loan can be 100% forgivable if at least 60% of the loan goes towards paying yourself—sometimes referred to as “owner’s compensation replacement.” You can meet this requirement by withdrawing loan funds weekly or monthly, and then “paying yourself” with them. These monthly or weekly withdrawals must equal the income you reported on your original PPP loan application. For example, if you reported that your take-home pay before the pandemic was $1,000 per week, then your loan withdrawals must roughly equal that amount.

You can view the SBA’s site for a full list of forgiveness-qualifying expenses.

It is very important to keep receipts of these qualifying expenses, so we recommend keeping your books up-to-date by depositing your loan in your Found account and using your Found card for automatic expense tracking. If you get audited, you can easily present all relevant documentation related to your PPP loan.

If you didn’t originally get your PPP loan deposited into your Found account, but want to move the funds over for easier expense tracking in preparation for applying for loan forgiveness, simply transfer the funds into your Found account. You can find your Found account and routing numbers by going into the “Profile” side menu in your app, tap on the “Business banking” tab, then select the “Direct deposit” option. Note: Found requires that you meet certain eligibility requirements in order to send your PPP loan to your Found account, and all loan payments must pass a compliance review. Not all loan payments are accepted. You can find Found’s eligibility requirements here.

If you are applying for your second PPP loan, you must also provide proof of the 25% reduction in gross income for one quarter of 2019 compared with the same quarter in 2020 to qualify for loan forgiveness. Your bank records will do the trick.

PPP Loan Tax Treatment

The federal government has issued guidance that PPP loan funds will not be subject to federal income tax, and all business expenses paid for with your PPP loan are still tax-deductible.

This means that if you use your $10,000 PPP loan to pay for supplies and office rent for your business, you can still deduct those business expenses on your taxes, but you don’t have to report that $10,000 on your tax return (or pay taxes on that money).

However, many states have their own state income tax rules governing PPP loans, so it’s important to check your state’s specific policies for PPP loan funds so that you aren’t surprised come tax time.

For a complete breakdown of state-by-state rules governing whether PPP loans are subject to income tax and/or are eligible to claim deductible business expenses against, check the Tax Foundation’s breakdown here. Tip: If you’re in Arizona, Florida, Idaho, Maine, Massachusetts, Minnesota, Nevada, New Hampshire, Texas, Utah, Vermont, or Virginia, you’ll want to make sure you’re reporting your PPP loan payment correctly on your state tax return.

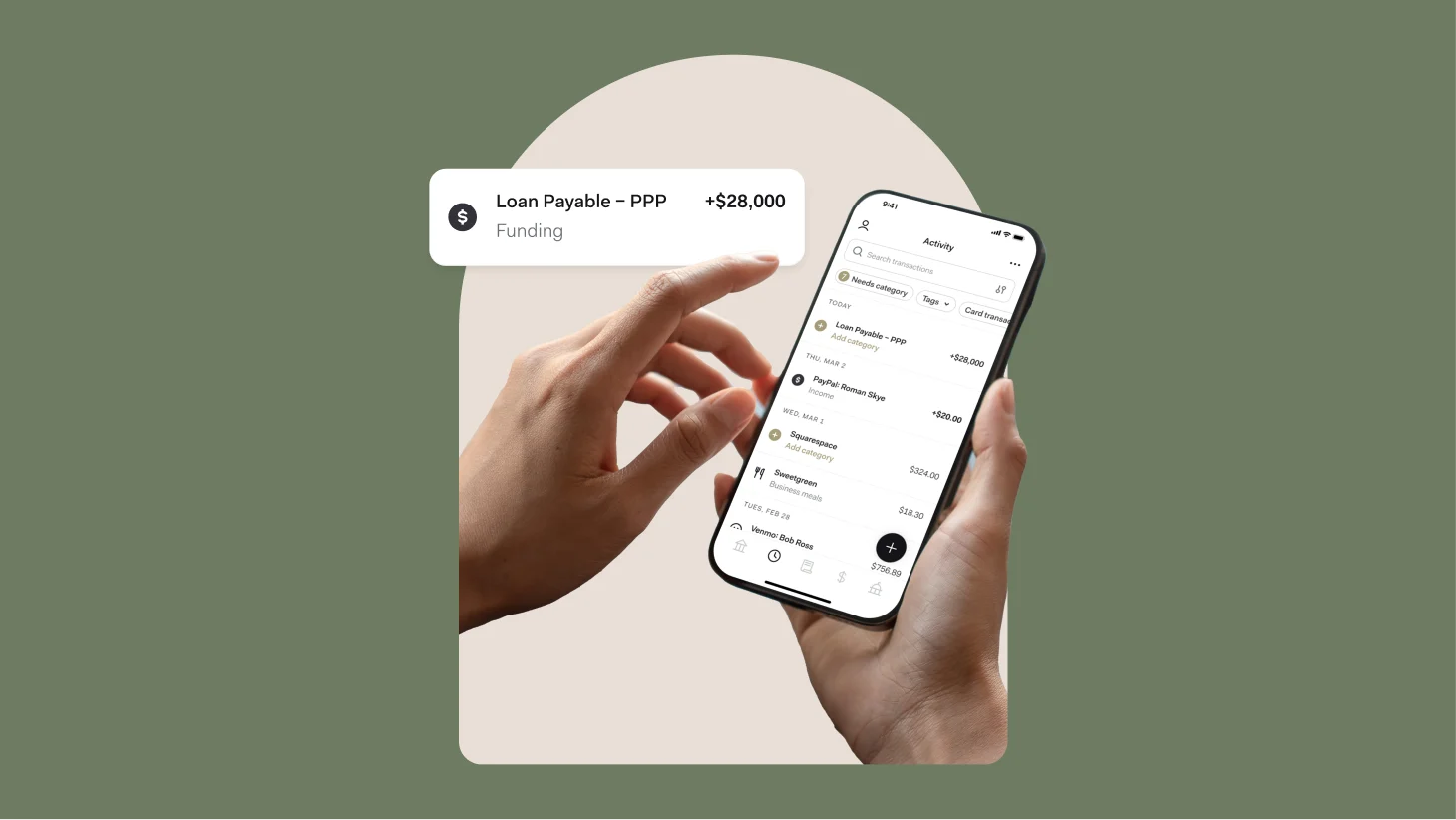

Finally, if you deposited your PPP loan into your Found account, ensure it’s been categorized correctly to reflect the expected taxes you will have to pay depending on where you live.

Most deposits to your Found account are categorized as “income,” rather than “funding,” so your tax bill can be updated automatically. Since PPP loans are not federally income-taxable and are indeed not income taxable in most states either, you’ll want to make sure you categorize these deposits as “funding” vs. “income.”

This will automatically adjust your tax bill estimate down, and reflect the fact that you’re not paying federal income tax on the PPP loan deposit. You can check the categorization of any deposit in your Found app by clicking into the deposit record, and checking if the deposit is listed as “Business Income” or “Funding.”

To change the categorization, simply tap on your deposit in your “Activity” log, tap the three dots in the upper righthand menu, and select “Mark as funding.”

Have more questions you want answered? You can read more about PPP loans at the SBA website.